Embedded Finance vs. Traditional Trade Finance: Side-by-Side

May 18, 2026

Embedded Finance vs. Traditional Trade Finance: Side-by-Side

When a US importer signs a purchase order with a Mexican injection molder, the money question hits within hours: who funds the 90-day gap between deposit, production, and final payment? For decades, the answer was a letter of credit from a global bank, a factoring line from a specialty lender, or a slow-moving SCF program negotiated at the treasury level. Today, a second answer has emerged — embedded finance — where working capital is offered inside the procurement, ERP, or B2B payments software the buyer and supplier already use.

The two models can fund the same shipment, but they behave very differently. Speed, cost, underwriting logic, user experience, and the type of supplier each can reach diverge sharply. For manufacturers in the middle of a [China-to-Mexico transition](China-to-Mexico transition), picking the wrong one can mean a 60-day delay in qualifying a factory or 200 basis points of margin lost on every container.

We at Reshore see this play out daily with clients reshoring plastic and tooling operations. This guide breaks down the side-by-side reality of embedded finance vs. bank-led trade finance, where each wins, and how to choose for a cross-border, USMCA-aligned program.

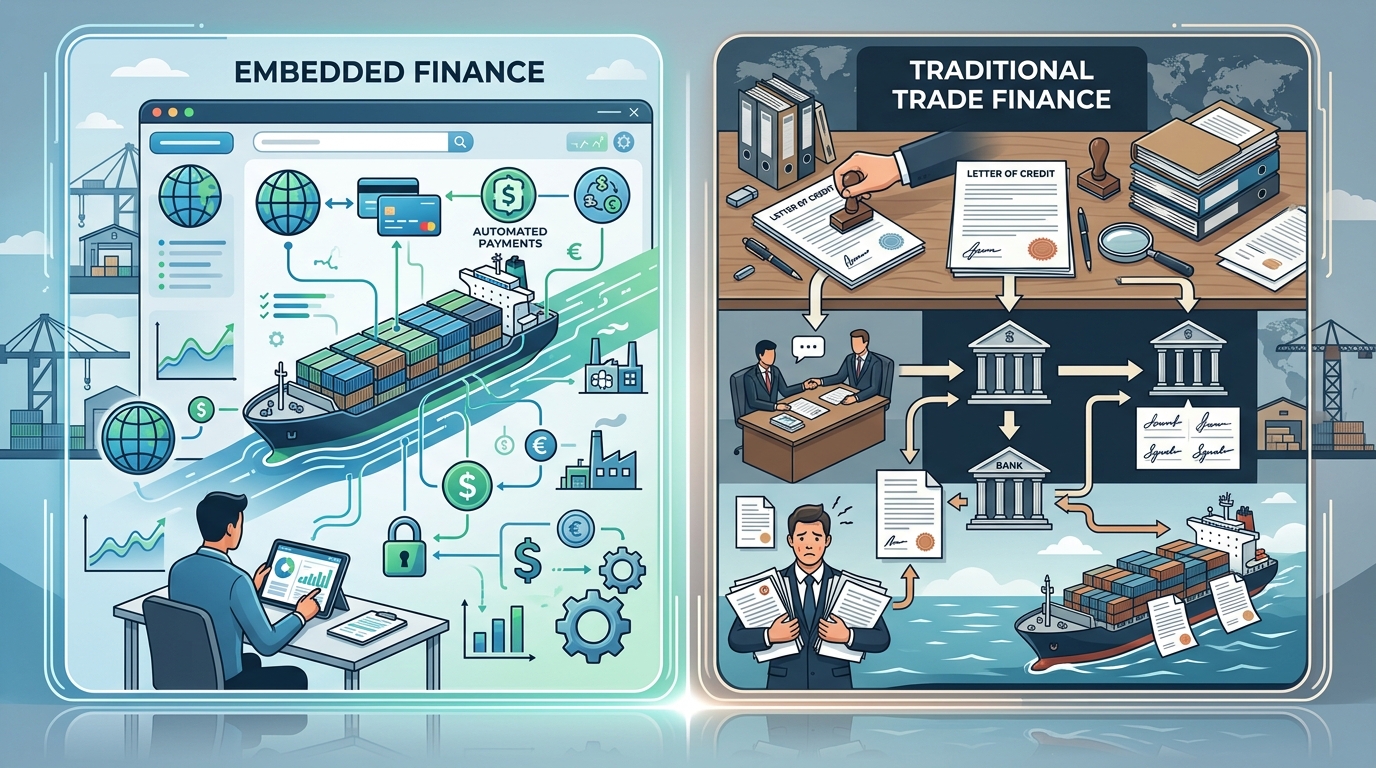

The Two Models in Plain Terms

Traditional trade finance refers to the instruments banks and specialty lenders have offered since the post-war era: letters of credit, documentary collections, bank-issued supply chain finance (reverse factoring), PO financing from non-bank lenders, and traditional invoice factoring. The capital comes from a regulated institution; the relationship is bilateral; the paperwork is heavy; and the underwriting is anchored on financials, collateral, and bank-rated counterparty risk. For a deeper foundation on these instruments, see the manufacturer's guide to trade finance instruments.

Modern trade finance, often described as fintech trade finance or embedded finance, refers to working capital products delivered inside another software layer — an ERP, a procurement platform, a B2B payments rail, a marketplace, or a vertical SaaS tool. Underwriting is data-driven (transaction history, invoice data, shipment events, ERP signals). Funding decisions arrive in minutes, not weeks. Capital sources are diverse: balance-sheet fintechs, bank-fintech partnerships, securitized funding vehicles, and increasingly, embedded credit programs from the platforms themselves.

Both models can finance the same purchase order. The difference is how they finance it.

Side-by-Side: Embedded Finance vs. Bank Trade Finance

| Dimension | Traditional Trade Finance | Embedded / Fintech Trade Finance |

|---|---|---|

| Onboarding time | 4–12 weeks (KYC, financials, collateral review) | Hours to days (API-pulled data, transaction history) |

| Underwriting basis | Audited financials, collateral, guarantees | Real-time ERP/invoice/transaction data |

| Approval speed per deal | 3–10 business days | Minutes to 48 hours |

| All-in cost (USD buyer, MX supplier) | SOFR + 250–500 bps + fees | SOFR + 300–700 bps, often flat fee structure |

| Document burden | Heavy (LC drafts, bills of lading, inspection certs) | Light (data flows; documents auto-attached from systems) |

| Minimum deal size | Often $250K+ for LCs; $1M+ for SCF programs | As low as $5K–$25K per invoice |

| Supplier reach | Established, bank-rated suppliers | Long-tail SMEs, including new Mexican factories |

| Currency handling | Strong for USD/EUR; weaker peso desks | FX often built in, transparent rates |

| Integration | Standalone bank portal, email, SWIFT | Embedded in ERP, procurement, or payments UX |

| Off-balance-sheet treatment | Available with auditor sign-off; legal review needed | Often pre-structured; varies by product |

| Best for | Large, repeatable trade lanes; LC-required jurisdictions | Speed, new suppliers, fragmented PO volume |

The pattern is consistent: banks bring scale, regulatory weight, and the lowest cost of capital when you can clear the eligibility bar. Embedded providers bring speed, breadth of supplier coverage, and a user experience that doesn't require a treasury analyst to operate.

Where Traditional Trade Finance Still Wins

Banks are not going anywhere. According to the International Chamber of Commerce's Trade Register, traditional trade finance instruments still underwrite the majority of cross-border B2B flows above the mid-market threshold. There are real reasons:

- Cost of capital at scale. For programs funding $50M+ in annual flow with investment-grade buyers, bank-led reverse factoring beats fintech pricing by 100–300 bps.

- Letter of credit jurisdictions. Some component categories, regulated imports, or first-time supplier relationships still require an irrevocable LC to give either side comfort.

- Sovereign and political risk wrapping. Ex-Im Bank and DFC programs, often layered onto bank LCs, are hard to replicate inside an embedded product.

- Auditor familiarity. A bank-led SCF program has well-established accounting treatment; some embedded products are still working through how CFOs and auditors classify them on the balance sheet.

If you're moving a high-volume, mature trade lane — say, a $30M annual injection molding program from an established Tier-1 in Monterrey — a bank-led SCF program is often the right answer.

Where Embedded Finance Pulls Ahead

The strengths show up exactly where reshoring programs live: new suppliers, fragmented POs, fast scale-up timelines, and cash flow that doesn't wait for a banker's calendar. Recent industry benchmarks on adoption and performance confirm that these strengths are now visible at the portfolio level, not just on individual deals.

1. Onboarding a brand-new Mexican factory

A first-time supplier in a growing cluster — Saltillo, Querétaro, Tijuana — often can't pass a major bank's KYC and credit review in the timeline a reshoring project demands. Embedded providers underwrite on transaction and operational data, which means a factory can be funding its first PO inside 10 days instead of 10 weeks.

2. PO-stage capital for the supplier

Traditional PO financing exists, but it's slow and expensive. Embedded PO financing, often triggered automatically when a buyer issues a PO inside a connected system, lets a Mexican producer buy raw resin, pay tooling deposits, and start production without dipping into its own working capital.

3. Dynamic discounting and early-pay programs

Embedded platforms make it trivial for a US buyer to offer early payment in exchange for a discount, with the supplier choosing per-invoice whether to accept. This is operationally impossible to run at scale through a bank portal.

4. Fragmented invoice volume

A buyer with 40 Mexican suppliers issuing 600 invoices a month doesn't want 600 documentary checks. Embedded invoice factoring processes the volume automatically, with exception handling rather than manual review. The landscape of providers and use cases has matured to the point where buyers can compare specialist players head-to-head on volume handling.

5. USMCA-aligned documentation

Modern platforms increasingly bake USMCA certificate-of-origin handling, HTS classification, and customs timing directly into the financing workflow — closing the gap between the financial event and the cross-border logistics event that triggers it.

The Hybrid Reality

In practice, most sophisticated reshoring programs run both. A typical structure:

- Bank-led SCF for the top 5–10 suppliers representing 70% of spend, where scale and cost of capital matter most.

- Embedded invoice finance and PO financing for the long tail — new factories, ramp-up suppliers, lower-volume specialty producers — where speed and reach matter more than pricing.

- Embedded dynamic discounting layered across both, captured as APR yield on excess cash.

This portfolio approach is what separates CFOs who treat financing as a strategic lever from those who still treat it as a procurement afterthought. For a deeper read on instrument selection, see our companion piece on Letter of Credit vs. Supply Chain Finance: Which Fits Your Reshoring Deal.

How to Decide for a Specific Deal

A practical decision tree we use with clients:

- Is the supplier bank-rated and the program above $10M annual flow? Start with bank-led SCF or LC.

- Is the supplier new, growing, or in an emerging cluster? Embedded PO finance or invoice factoring will move faster.

- Is the buyer's priority margin capture on early pay? Embedded dynamic discounting wins.

- Does the deal cross a regulated category (medical, defense, food)? Likely an LC is still required regardless.

- Is the program scaling from 5 to 50 suppliers in 12 months? Embedded is the only model that scales operationally.

The wrong move is to assume one model fits the entire portfolio. The right move is to map each supplier tier to the financing instrument that fits its risk, size, and lifecycle stage.

What This Means for Reshoring Programs

Financing isn't a back-office function in a China-to-Mexico transition — it determines which factories you can qualify, how fast you can move tooling, and how much of your landed cost advantage survives. The rise of software-native working capital has materially expanded the universe of Mexican suppliers a US buyer can practically work with, because it removes the bottleneck that used to keep small and mid-size factories out of formal trade finance entirely.

That doesn't make traditional trade finance obsolete. It makes the choice strategic. The manufacturers winning at nearshoring are the ones treating embedded finance and bank trade finance as complementary tools in a working capital stack — not as a binary choice.

If you're evaluating a reshoring move and trying to figure out which financing structure fits your supplier portfolio, tooling timeline, and cash flow profile, we can help map it.

Frequently Asked Questions

Q: Is embedded finance cheaper than a bank letter of credit?

Not usually on headline rate, but often cheaper on total cost when you include onboarding time, document handling, and the opportunity cost of delayed shipments. Banks typically win on raw cost of capital for large, mature programs; embedded finance wins on speed, supplier reach, and operational overhead for fragmented or fast-moving portfolios.

Q: Can embedded finance handle USMCA documentation requirements?

Increasingly, yes. Leading fintech trade finance platforms integrate USMCA certificate-of-origin handling, HTS classification, and customs broker workflows directly into the financing trigger, so the financial event aligns with the cross-border logistics event. Buyers should still validate that the platform's documentation meets their customs counsel's standards.

Q: What is the main difference between embedded finance vs. bank trade finance?

The core difference is where the capital lives in your workflow. Bank trade finance is a standalone product accessed through a portal or relationship manager; embedded finance is delivered inside the software you already use — ERP, procurement, or B2B payments — with underwriting driven by real-time transaction data rather than periodic financial reviews.

Q: Are embedded finance products treated off-balance-sheet?

It depends on the structure. Many embedded reverse factoring and dynamic discounting products are designed to qualify as trade payables rather than debt under US GAAP, but the treatment hinges on specific terms — recourse, supplier election, payment timing. Always run the structure past your auditor before assuming off-balance-sheet treatment.

Q: Does Reshore help with arranging trade finance for reshoring projects?

Reshore focuses on the operational backbone of reshoring — tooling transfer, AI-powered supplier matching, factory sourcing, and logistics — and works alongside the trade finance providers, banks, and embedded platforms our clients select. We help clients structure supplier relationships and payment terms in ways that make them financeable under either model.

Q: How long does it take to set up embedded finance for a new Mexican supplier?

Onboarding typically runs from a few hours to two weeks, compared with 4–12 weeks for a traditional bank facility. The speed comes from API-based data pulls from ERPs, accounting systems, and shipment platforms, which replace the document-heavy underwriting cycle of a bank.

Q: When should I still use a letter of credit instead of embedded finance?

Use an LC when the supplier or jurisdiction requires it for legal or risk reasons, when the transaction is a one-off large-ticket deal with an unfamiliar counterparty, or when sovereign-risk wrapping (Ex-Im, DFC) is part of the structure. For repeat flows with known suppliers, embedded products are almost always faster and lighter.

Q: Can a small Mexican factory qualify for embedded finance more easily than for a bank line?

Generally yes. Embedded providers underwrite on transaction data, buyer creditworthiness, and operational signals rather than the audited financials and collateral that banks require, which makes them well-suited for small and mid-size Mexican producers in growing industrial clusters who would otherwise be locked out of formal trade finance.